It’s Not Easy Being Green

Clarke McEwan Accountants

It’s Not Easy Being Green

Climate change featured heavily during the election and now the Albanese Government is putting into place some of the promises it made. We look at the current state of play and the likely impact.

The Government’s Climate Change Bill passed the House of Representatives in early August and is now before the Senate Environment and Communications Legislation Committee for review. But what impact does the legislation have on business and consumers in Australia?

Under the Paris Agreement, a legally binding international treaty, Australia and 192 other parties committed to substantially reduce global greenhouse gas emissions to limit the global temperature increase in this century to 2 degrees Celsius while pursuing efforts to limit the increase even further to 1.5 degrees. At this level, the more extreme impacts of climate change - floods, heatwaves, rising sea levels, threats to food production - can be arrested. As part of this commitment, the parties are required to communicate their emissions reduction ambitions through a Nationally Determined Contribution (NDC). On 16 June 2022, Australia communicated its updated NDC to the UN, confirming Australia’s commitment to achieve net zero emissions by 2050, and a new, increased target of 43% below 2005 levels by 2030 (a 15% increase on the previous target). The Climate Change Bill enshrines these emission targets into legislation.

The Bill itself sets an accountability framework for climate targets but does not introduce mechanisms to cut emissions.

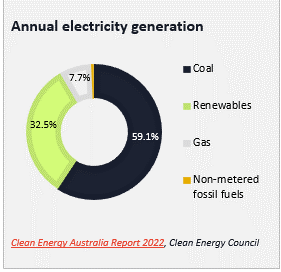

Impacted industries

The energy sector is at the heart of climate change producing around three-quarters of global greenhouse gas emissions. In Australia, the CSIRO says energy contributes approximately 33.6% of all emissions, with a further 20.54% from stationary energy (from manufacturing, mining, residential and commercial fuel use), transport 17.6%, and agriculture 14.6%. The future of the energy industry is also at the crux of the Government Powering Australia policy.

Emissions reduction is not just a social obligation but a necessity as investment tilts towards lower emission suppliers. As an example, the 2022-23 Federal Budget committed a $120 billion 10-year infrastructure pipeline. The June 2022 Business Council of Australia Infrastructure in a world moving to net zero report provides a series of recommendations to address the way in which Government invests including the adoption of low carbon materials on public projects and options for reducing emissions during construction, understanding the whole of life emissions impact of infrastructure projects and potentially adopting the UK style PAS2080 standard on carbon management infrastructure, and a shift in procurement to lower carbon supply chains. If these considerations have not made it into business production and supply chain planning, they will soon.

Amongst other initiatives the Government have committed to:

- $20bn investment in Australia’s electricity grid to accelerate the decarbonisation.

- An additional $300m to deliver community batteries and solar banks across Australia.

- Up to $3bn investment in the new National Reconstruction Fund to support renewables manufacturing and low emissions technologies.

- Powering the Regions Fund to support the development of new clean energy industries and the decarbonisation priorities of existing industry.

- Double existing investment in electric vehicle charging and establish hydrogen refuelling infrastructure (to $500m).

- Review the effectiveness of the Emissions Reduction Fund that provides businesses with the opportunity to earn Australian carbon credit units for every tonne of carbon dioxide equivalent a business stores or avoids emitting through adopting new practices and technologies.

- New standardised and internationally aligned reporting requirements for climate risks and opportunities for large businesses.

- Reduce the emissions of Commonwealth Government agencies to net zero by 2030.

In essence, business can expect directed funding for co-investment in emission reduction technology, Government spending to be through the lens of the renewed emissions targets, and for new funding opportunities to advance low emission technology.

But emissions reduction is not just about industry. Land use change can have a significant impact on emissions through reductions. For example, a reduction in forest clearing in 2020 reduced emissions by 4.9%. One initiative needs to go hand in hand with the other.

Renewables increased 5% on 2020 contributed by small scale solar, and large scale solar and wind farms.